A market poised for expansion

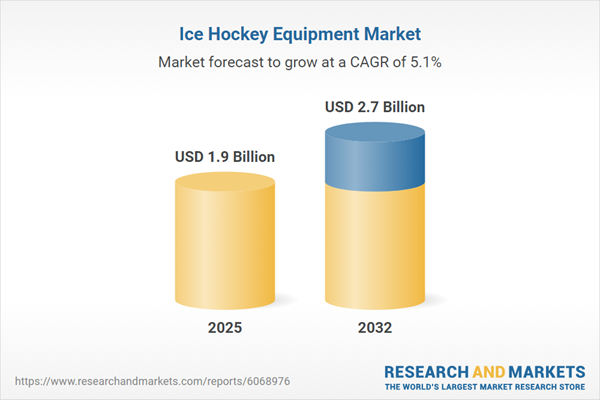

The global ice hockey equipment market is on track to climb from roughly $1.9 billion in 2025 to $2.7 billion by 2032, reflecting a compound annual growth rate of about 5.1 percent. This trajectory signals not only steady financial gains but also a reshaping of the sport’s gear landscape.

Central to this evolution are a series of technological breakthroughs that are redefining performance and safety standards. Advanced composites now dominate stick construction, delivering lighter frames with customizable blade curves and flex ratings that cater to individual player preferences. Skates have been transformed with thermoformable boots, carbon‑infused outsoles and enhanced ankle support, while helmets increasingly embed smart sensors that monitor impact force and head acceleration in real time.

Materials such as D3O are being incorporated into pads and gloves, offering superior shock absorption without adding bulk. Meanwhile, 3D scanning and printing enable manufacturers to produce equipment that fits each elite player’s anatomy with unprecedented precision. These innovations are not confined to the professional tier; they filter down to amateur and recreational segments, where demand for high‑quality yet affordable gear is expanding the mid‑range product line.

Geographically, North America remains the largest consumer of ice hockey equipment, driven by strong participation in the United States and Canada. Europe follows as a vibrant secondary market, with Sweden, Finland, Russia, the Czech Republic and Switzerland contributing to a steady rise in sales. At the same time, the Asia‑Pacific region is emerging as a new hotspot, particularly in China and South Korea, where youth programs and growing female involvement are unlocking fresh demand channels.

The demographic shift toward younger players, women’s hockey and recreational leagues is reshaping product development pipelines. Manufacturers are responding with gear specifically engineered for female athletes and for school‑based training programs, while subsidized equipment initiatives and public‑private partnerships aim to broaden access. This diversification of end‑users fuels a broader base of consumption beyond the traditional elite player market.

Looking ahead, the convergence of material science, digital monitoring and expanding market reach suggests that the ice hockey equipment sector will continue to innovate and capture new revenue streams. Companies that can blend cutting‑edge technology with targeted marketing to emerging demographics are likely to secure the most pronounced gains in the coming years.